Do You Need Surrogacy Insurance As a Surrogate?

Do You Need Surrogacy Insurance?

Yes, but not in the way you might think.

You do not need a policy that will cover a surrogate pregnancy (which we call “surrogacy-friendly”) upfront. In fact, your surrogacy insurance is not typically used until a pregnancy is confirmed. Some intended parents may have employer-sponsored plans that offer IVF and/or surrogacy-related benefits before pregnancy, but that is relatively rare.

While you do need coverage for the pregnancy itself, it does not have to come from your current plan. Many insurance policies have surrogacy exclusions, which means they will not cover services related to a surrogate pregnancy. That is one reason insurance review is such an important part of the process. Even when a policy does not have an exclusion, coverage can change from year to year or based on changes to your employment or plan.

That’s why Heartland Surrogacy requires a policy that covers the surrogacy pregnancy, but if you do not already have one, we will help you find one. Depending on the time of year and your personal circumstances, there may be options available through the Marketplace or through trusted insurance brokers.

Why Insurance is Required in Surrogacy

A surrogacy-friendly insurance policy is one of the biggest financial and medical safeguards in a journey. It helps protect the surrogate, the intended parent(s), and the pregnancy.

Some agencies offer lower compensation to surrogates who do not have surrogate-friendly insurance. At Heartland Surrogacy, we provide you with information on typical compensation and allow you to set your own amounts. This can vary based on your personal goals and family circumstances. We do not automatically lower compensation based on the status of your health insurance.

If we think the combination of base compensation and insurance costs – two of the largest expenses in a journey – could extend your wait time for a match, we will let you know and talk through your options together.

How We Help You Navigate Insurance

We know insurance can be confusing, and we don’t expect you to know whether your plan is “surrogacy-friendly.” When you apply with our agency and begin the pre-screening process, your policy will be professionally reviewed. That review looks for clear surrogacy exclusions, details about maternity coverage, relevant fine print, and any additional paperwork that may be required.

We will share this information with potential IPs so they can plan for the financial side of the journey. IPs are also made aware that policies can change from year to year, and that it’s possible for a surrogate’s personal coverage to be dropped. We let them know to be prepared to purchase a surrogacy-specific plan if this happens.

If a current policy is found to be surrogacy-friendly, it can usually be used for services after a pregnancy is confirmed and care beings with a regular obstetric provider. If your policy will not cover a surrogate pregnancy, we will connect you with an insurance broker to look for a suitable policy on the Health Insurance Marketplace. However, Marketplace policies can only be purchased during open enrollment, which typically happens near the end of the calendar year. Availability also varies greatly by county and can change from year to year.

If you are outside that window or there are no suitable options available, the IPs will need to purchase a surrogacy maternity plan through an insurance broker. This type of plan is often a negotiated package for services that is backed by insurance.

When researching insurance options, we will gather information from you about your provider preferences and the services offered in your area. While we will work hard to find a policy that includes your preferred providers, some flexibility is sometimes necessary.

Our goal is to make this process feel manageable.

Who Pays for Surrogacy Insurance?

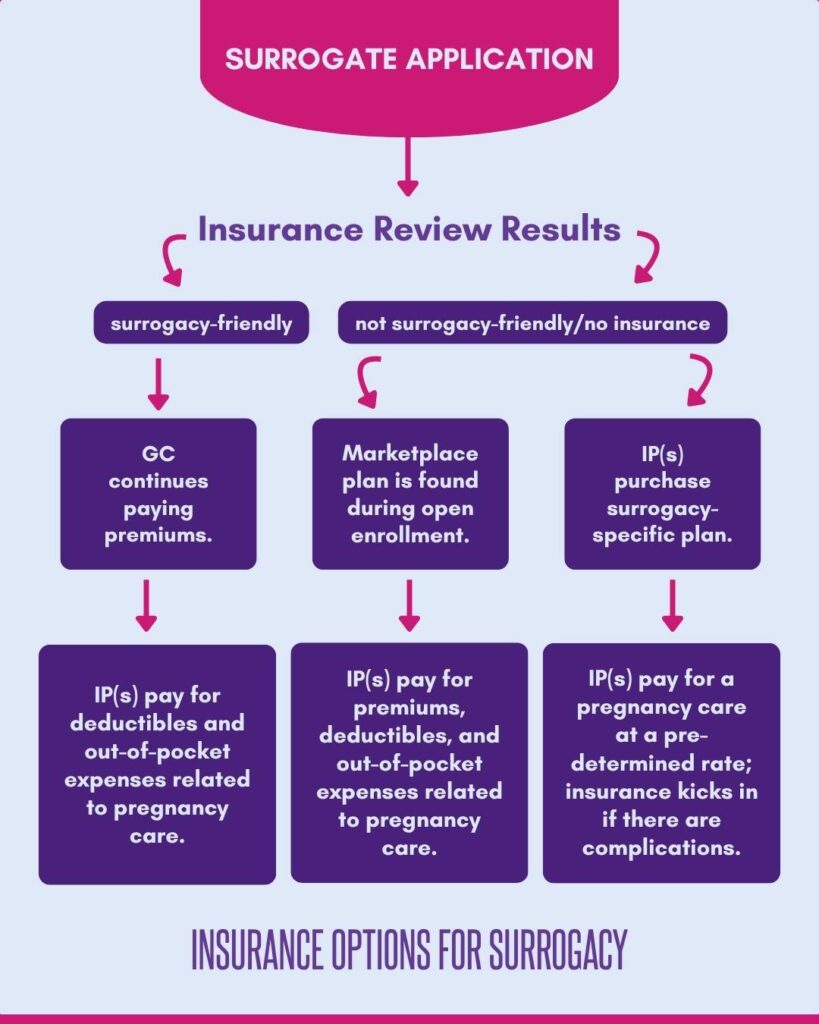

Intended parents are responsible for all expenses related to the surrogacy journey. When it comes to insurance policies, there are generally three paths:

- Your current insurance policy is surrogacy-friendly, so you continue paying your regular premiums as usual and the IP(s) are responsible for deductibles and out-of-pocket expenses related to pregnancy care.

- A Marketplace policy is purchased specifically for the surrogacy journey, and the IP(s) are responsible for the premiums, deductibles, and out-of-pocket costs associated with the pregnancy.

- The IPs purchase a surrogacy-specific plan, which typically means that they will make payments to providers at a predetermined rate. Insurance coverage will kick in if complications arise.

As with other expenses in a surrogacy journey, there may be times when you pay for a balance upfront and then are reimbursed by the IPs, typically through the escrow account.

You Don’t Need to Have It All Figured Out

You don’t need perfect insurance to apply to become a surrogate, and you don’t need to have all the details to get started. Insurance coverage is required for surrogacy, but it’s just one of the many logistical details that our team will help you figure out.

From reviewing a current policy to helping you find a new one, this is exactly the kind of work we’re here for!

Take the First Step Toward Becoming a Surrogate

We know there is a lot to learn about becoming a surrogate. By filling out the form below, you can set up a consultation with our team to learn more or begin your application if you’re ready.

We’ll give you the information you need to feel empowered in your journey and continue to guide and support you along the way.